Alan Kohler’s Quarterly Essay is a valiant attempt to put the housing crisis into a historical and macroeconomic perspective. He offers solutions, but there are no quick fixes. Kim Wingerei with the review.

It’s the crisis everyone wants to talk about that politicians avoid addressing, and property owners profit from. It’s a crisis that has been decades in the making and will take decades to fix.

Without saying so, Alan Kohler recognises that the main obstacle is indeed the political will. “It won’t be enough simply to restore the amount of housing construction to what it was before the pandemic, as the federal government is now aspiring to do.” In the scheme of things, the pandemic was merely a blip in the long-term trend.

We don’t need another inquiry or a royal commission; there’s a room full of inquiries, reports and submissions.

Alan Kohler has been writing and talking about the economy for a long time. He is well respected and has a knack for explaining complexities in terms we can all understand. He also knows how to employ a bit of nostalgia to tug on the reader’s heartstrings. The introduction of his 86-page essay takes us back to his own parents, who bought a piece of land in South Oakleigh outside Melbourne for £1000 in 1951. The house cost them another £1250, all up roughly $121,000 in 2024 dollars. He describes how “Dad built the house himself, including making the bricks, working on weekends and at night, and Mum and Dad lived in a garage.”

The important point he makes is that the cost of the house would have been approximately 3.5 times their median income. And that ratio hadn’t changed all that much when Alan and his wife bought their first house in 1981 for around $40,000 ($215,000 in 2024 dollars). The ratio stayed steady for another 20 years.

Fast forward to August 2023, “the median Australian house price was $732,886, which was 7.4 times annualised average weekly earnings.”

From 3.5 times the median income to 7.4, that’s the housing crisis in a nutshell. And it all started changing at the beginning of the millennium.

House prices and wages (full-time weekly earnings, index: 1970 = 100). Source: Business Insider.

Winners and losers

There are winners and losers in every crisis. The winners are property owners and real estate developers, as well as State Governments who benefit from more stamp duty as property prices rise. The losers are the Federal Treasury deprived of CGT tax dollars and “those born after 1983 – the millennials who were just becoming adults when they grew into their generational label in 2000 at the same time house prices started taking off.”

Kohler goes into significant detail exploring the realities of housing affordability, and how it impacts in different ways on people depending on our income and where we have chosen to live – or cannot afford to live. The latter point is important, as one of the consequences of reduced affordability for middle-income city dwellers is that they have to move further and further away from the CBD if they want to trade up without paying more for their housing.

“…to get a three-bedroom family home now, if that couple who bought 35 Foch Street, Box Hill South in 2012 are still earning 2.6 times average weekly earnings, they would need to be looking another 10 kilometres away from the CBD, in Bayswater, Lalor or Tarneit.”

In short, Alan contends that:

Australian homes have simply become too expensive for society to work normally.

It has become a vicious circle, higher house prices lead to declining home ownership, forcing more people to rent, while not enough properties are built for the rental market, forcing rents up due to lack of supply. “In many suburbs, rents have risen so much that it’s becoming more expensive to rent.”

Housing Crisis: forsake the Future Fund Albo, you’ve already found a better build

How (and when) did it go so wrong?

The housing crisis is an issue of supply not meeting demand, leading to higher prices.

One of the most fascinating chapters in the Essay is the historical context. Although the crisis is happening now, Alan goes into detail about how “the treatment of land in Australia’s first century created the conditions and attitudes that led to the housing crisis of its third century.”

He highlights three primary issues that got us to this point.

The lack of public housing

“Between 1947 and 1961, the housing stock in Australia increased by 50 per cent, about 10 per cent more than the increase in population.” About a quarter of that was built by the Government through programs such as the Commonwealth–State Housing Agreements (CSHA). But it also led to an overemphasis on the virtues of home ownership, it “had been elevated to an almost religious status.” By 1971, 40% of the houses built under the CSHA had been sold into private ownership.

By the time Malcolm Fraser was elected in 1975, the idea of public housing had been dismissed as a “form of welfare for the neediest.” By 1982, the CSHA built just over 7,000 houses. Since then, public housing has been more of a subject of campaign speeches and broken promises than actual action. Hawke promised 145,000 in 1983, and Albanese 1.2 million over five years in 2023 – aspirational targets not backed up by substantive policies to achieve them – more on that later.

Australia is not unique in this regard, of course, but many other countries have taken a very different approach over the post-war years and with great success. Austria is one such example.

Australia’s crowded sprawl

Despite our vast lands, Australia has one of the most concentrated populations in the world. Kohler highlights that “if you include all cities, not just capitals, 91.9 per cent of Australians are urbanites, so less than a tenth live in the bush.” It was 70% in 1950, and the global average is 62.8%, according to data produced by the World Resources Institute.

There are, of course, good reasons for that, including the fact that much of those lands are deserts or too dry for sustainable community establishments. Add to that the enormous distances between places, which makes transport costly, and “if you don’t live in a city, you have a long trip to get to a doctor or a decent supermarket.”

Good intentions to decentralise have been around for over a century, but “most of it was political lip service.”

This extreme centralisation has, however, led to congestion and less housing being built where people want it. Compounding this issue is the severe lack of public transport infrastructure, probably one of the major long-term policy failures of post-war governments – both on federal and state levels.

What no government, state or federal, has ever done, is properly invest in fast railway services from regional centres to the cities.

Kohler is not here talking about the numerous plans for very fast inter-city trains, plans yet to be executed, but “just reasonably fast, reliable trains that could get from Newcastle to Sydney, or Bendigo to Melbourne, in less than an hour.”

He also discusses at some length the issues of our reliance on car transportation in cities that “were not fully developed before the car arrived.” This passage struck me as particularly poignant:

Demographer Simon Kuestenmacher tells me that the urban sprawl in Australia is the reason there is little to no medium-density housing, and is entirely due to affordable cars arriving before the cities were fully developed, so that families, including the immigrants from crowded Europe and the United Kingdom, were able to build on large blocks, four or five to an acre. “And once you do that,” says Kuestenmacher, “how do you add medium density?”

The lack of state and local government planning

Here, Kohler goes into detail about the various (failed) attempts at making state and local governments accountable for long-term planning ow how much to build, where to build and how to build. He is particularly scathing about zoning regulations.

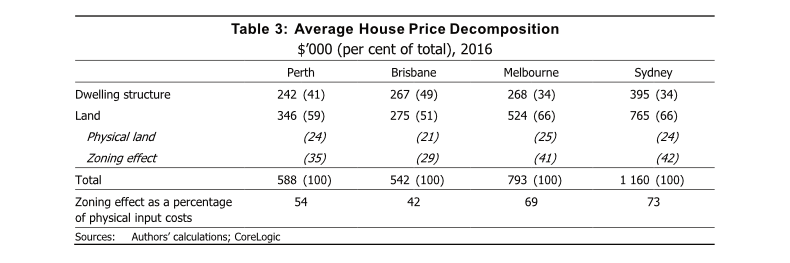

He refers to a 2018 report by Reserve Bank economists Ross Kendall and Peter Tulip in which they calculated the impact of zoning on house prices. The report was widely publicised at the time, and although the analysis is not for the faint-hearted, the key finding of the report was quite straightforward:

…without zoning, and the restriction on land supply that results from it, houses would be an average of 36.8 per cent cheaper in those four cities.

The four cities being Perth, Brisbane, Melbourne and Sydney.

In Kohler’s view, the lack of uniform and consistent urban planning and zoning resulted in “any attempts to address housing need through the planning system only happened as a result of piecemeal, local initiatives.”

“The result has been that Australian cities have turned into sort of ‘reverse donuts’ – high-rise apartments in and around the CBD and then low-rise (single dwellings) as far as the eye can see, with a few exceptions.”

Anyone who has ever had to go through an urban planning process will get a good chuckle out of Kohler’s depiction of how it works – or rather, doesn’t.

It is important to note that Kohler’s criticism of councils is about planning, not approvals. The latter is often touted as the root cause of the problem, frequently cited by federal politicians. In a recent article in The New Daily, fellow economics writer par-excellence Michael Pascoe makes short shrift of this particular furphy, pointing out that approval numbers (or timeliness) are not the problem and that there are generally more approved projects in the system than there are actual projects under construction. Kohler concurs but also highlights how developers are apt to “sit on” approvals as prices rise to maximise profits.

In an earlier review of the essay in Crikey, occasional MWM contributor Cameron Murray refers to another aspect of the council planning conundrum. He points out that the ‘cartel’ of bankers and developers is “broadly in support of removing council regulations, which apparently make homes cheaper,” making the point that if the cartel wanted prices to be higher they’d “support more council regulations, not fewer.”

Counterpoint from Koukoulas

We sought comments from economist and commentator, Stephen Koukoulas, who offered a different take on rental prices in particular:

In terms of the rental market, there is no evidence that dwelling rents are particularly unaffordable. To be sure, rents in the last two years have risen quickly, and rental vacancy rates in most capital cities are presently very low, but over any length of time, rents have risen at a pace below that of wages, which points to a sustained long-run improvement in rental affordability.

Over the past 5 years, for example, dwelling rent has risen 9.8 per cent, while the wage price index has risen 13.6 per cent. Over 10 years, rents are up 17.0 per cent, with wages up 27.5 per cent. Over 25 years, rents are up 104 per cent, while wages are up 114.4 per cent.

Koukoulas also offered nuance around how the reduction in the homeownership ratio has come about, saying that “over that time frame [it] is potentially linked to social issues including more divorces, later cohabitation as young folk undertake more study, education and training. Not [just] the price of dwellings.”

He is less concerned about house prices than Kohler, suggesting that the problem “might not be all that big and [the fix] might not work at all if it is non-financial reasons that have impacted on homeownership rates.”

Housing demand and negative gearing

Lack of supply is a long-term problem to solve, but the Gordian Knot of housing affordability is changing the root cause of spiralling demand that makes housing such an attractive investment. As Kohler points out in his introduction, the demand for housing started taking off in earnest after the Howard Government’s reduction of the capital gains tax (CGT) by 50% in 1999.

This was further fuelled by the (resumption) of first home buyer grants and consecutive interest rate cuts between 2001 and 2003, which, together with the ‘Dotcom Bubble’ sharemarket crash of the year 2000, meant that “investors rushed from shares to property, funded by cheap debt.”

Then came a tripling of net migration between 2003 and 2009. Nothing wrong with immigration, but it was never matched with any forward planning to meet the added demand for housing.

As population increased, housing construction stayed the same, and didn’t increase until the late 2010s.

However, the combination of negative gearing (where property owners can deduct the interest paid on loans from rents earned) and the reduction of the CGT was the real rocket fuel of house values and rental costs.

Established house price index and CPI. Source: Department of Parliamentary Services.

This was, of course, also reflected in the debt- and price-to-income ratios, the latter increasing from 1:1 in 1986 to 5:1 by 2009.

Kohler also points out that the Reserve Bank’s enduring obsession with an inflation target of 2 to 3% has been “disastrous because of the way it distorted decision-making and house prices, and absurd because an inflation rate of 1 to 2 per cent, as it was after the GFC, is not dangerous in the way an inflation rate of 5 to 6 per cent can be.”

Rising house prices and rents are great for those who own houses and investment properties, but not so good for those wanting to buy their first home or rent in places where demand outstrips supply. Removing negative gearing and increasing the CGT may well reduce valuations and rents but won’t increase demand, and could amount to political suicide for the Government that dared even to suggest it.

That’s the impossible knot to disentangle.

Solutions

As a result of the aforementioned RBA analysis of zoning’s effect on housing prices, a report titled The Australian Dream: Inquiry into Housing Affordability and Supply in Australia, was published by the Parliamentary Standing Committee on Tax and Revenue in 2022. It focused on the supply issues, with dissent from the Labor members of the committee who wanted the focus to be on demand. As always, tribalism does not often lead to sensible consensus or solutions.

Anthony Albanese’s Labor Government is continuing to focus on demand, or rather aspirations of demand, by setting a target of 1.2 million new dwellings in five years. It’s the States who have to make that happen, though, with an offer of $15,000 paid per block of land built on, paid by the Federal Government, capped at $3B, or 200,000 new houses, leaving a 1 million shortfall between aspirations and reality,

There is also an “issues paper” on housing in the works by the Department of Social Services, indicating that “the government is coming at it as a welfare issue rather than an economic one.”

And let’s not forget the HAFF.

From Main Street to Wall Street: is the HAFF housing scheme a gift to the money men?

In short, there are no real, substantive long-term solutions on the table. As Kohler points out:

The politics of it is both simple and difficult: housing is a cartel of the majority, with banks and developers helping them maintain high house prices with the political class actively supporting them.

Kohler is adamant that we first need an agreed aim, and that this aim must focus on the real problem, that “the price of housing is now twice the multiple of income it used to be,” and that “any serious effort to deal with housing affordability should be explicitly aimed at getting that ratio down and keeping it there.”

In addition, the emphasis on housing as a primary source of wealth for Australians needs to change in Kohler’s view. One way to do that is by making other alternatives (superannuation, share investments, etc.) equally attractive and accessible for the many, not just the fortunate few.

But it also requires changes to CGT discounts and limitations on negative gearing, as well as making sure that immigration targets are linked to realistic targets of new housing builds, with achievable (and properly funded) incentives to increase supply.

Kohler goes into more detail about the various ways the overall aim can be achieved, including removing the stranglehold that the property and banking cartels have on the supply side.

Federal and State Governments also need to combine efforts to plan for a sustainable future of fewer cars and more public transport where it is most needed in and around the outskirts of the CBD’s.

There are solutions to the property crisis, but it will take time, political will and stamina, change in attitudes, and significant public investment in both supply and infrastructure.

To achieve this will require active, and serious, government intervention.

And reading Alan Kohlers’s excellent essay.

THE GREAT DIVIDE – Australian Housing Mess and How to Fix it – Alan Kohler – Quarterly Essay 92.